I. 글로벌 항공 산업에서 좌석 효율성이 갖는 경제적 의미

전 세계 항공 여객 시장은 연간 약 50억 명 규모이며, 매출은 약 1조 달러에 달한다. 이는 항공 산업이 단순한 운송 산업을 넘어, 글로벌 경제의 핵심 인프라임을 의미한다.

이 시장에서 항공사의 수익성을 좌우하는 핵심 요소는 기단 규모나 운항 횟수가 아니라, 고정된 기내 공간을 얼마나 효율적으로 활용하느냐에 있다. 항공기 동체는 한 번 제작되면 쉽게 확장할 수 없는 한정 자산이다.

좌석 배치 방식 하나의 차이는 대형 항공기 한 대당 연간 수천만 달러 규모의 수익 격차를 만들어낸다. 이 효과는 장거리 노선에서 더욱 극대화되며, 프리미엄 좌석이 전체 수익 구조를 좌우하게 된다.

프리미엄 좌석은 단순한 서비스 옵션이 아니라 장거리 항공의 수익을 견인하는 핵심 엔진이다. 비즈니스 클래스 좌석 1석이 창출하는 수익은 이코노미 좌석 여러 석의 합보다 크다.

그러나 기존 기내 설계 방식은 구조적 한계에 부딪혀 있다. 좌석을 넓히면 좌석 수가 줄고, 좌석 수를 늘리면 서비스 경쟁력이 약화되는 제로섬 구조에 갇혀 있기 때문이다.

좌석 효율성 혁신은 이 한계를 근본적으로 해소한다. 공간을 수평이 아닌 3차원적으로 재해석함으로써, 항공기 구조 변경 없이도 프리미엄 좌석 수용 능력을 확대할 수 있다.

이 방식은 운영비 증가 없이 순수한 매출 상승 효과를 창출한다. 기내 레이아웃은 더 이상 비용 요소가 아니라, 전략적 수익 레버로 전환된다.

결국 좌석 효율성이란 디자인의 문제가 아니라 재무 전략의 문제다. 공간이 재정의되는 순간, 항공기의 가치 역시 새롭게 정의된다.

이 차트는 전 세계 항공 여객 매출의 기본 시나리오(Baseline)와 좌석 효율성 개선 시나리오(+12%)를 시간 경과에 따라 비교한 것입니다. 동일한 수요 성장률을 가정하더라도, 좌석 효율성이 개선되면 매년 전체 매출 곡선 자체가 더 높은 수준으로 상승하게 됩니다. 이는 2030년경에 이르면 연간 매출 차이가 약 1,300억 달러(한화 약 170~180조 원)에 달할 것임을 시사합니다. 이것은 단순히 비용을 절감하는 차원의 문제가 아닙니다. 이 지표는 객실 공간의 효율성이 매출 기반 자체를 직접적으로 확장시킨다는 사실을 보여줍니다.

II. 왜 게임 체인저인가? – 대한항공 A380 사례

대한항공 A380의 2층(상부 데크) 기체 폭은 약 5.8m다.

중앙 복도 폭을 여유 있게 1.2m로 확보하더라도, 양쪽 좌석 구역에는 각각 약 2.3m의 폭을 확보할 수 있다.

이는 현재 어떤 프리미엄 좌석보다도 길고 넓은 공간을 설계할 수 있는 조건이다.

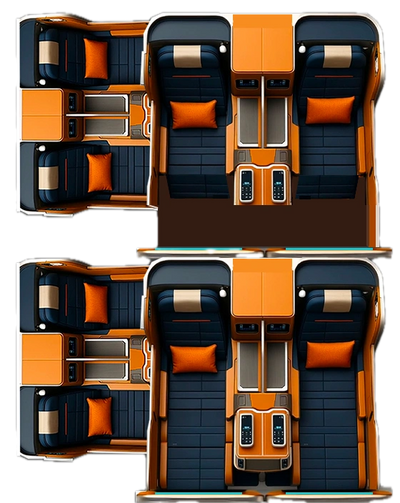

예를 들어, 가로 1.9m × 세로 2.3m의 공간 안에 4석 구조의 공간 효율형 비즈니스석을 배치할 경우,

기존 비즈니스 클래스보다 더 여유로운 개인 공간을 제공하면서도 좌석 수는 오히려 증가시킬 수 있다.

실제로 대한항공 A380 상부 데크의 기존 비즈니스석은 94석이지만,

공간 혁신 좌석을 적용하면 최대 136석까지 설치가 가능하다.

이는 기체 변경 없이 프리미엄 좌석 수를 약 45% 증가시키는 구조적 전환이다.

또한 좌석 규격 측면에서도 개선 효과가 뚜렷하다.

대한항공 기존 비즈니스석의 규격이 길이 188cm × 폭 53cm인 반면,

공간 혁신형 좌석은 길이 190~230cm, 폭 60~70cm 수준의 더 넉넉한 개인 공간을 제공할 수 있다.

같은 기체, 같은 노선, 같은 운항 비용에서

좌석 설계만 바꿔도 ‘프리미엄 경험’과 ‘수익성’을 동시에 높일 수 있다.

이것이 바로 공간 재해석이 만들어내는 ‘공간의 마술’이며,

A380 상부 데크 공간 혁신 좌석이 ‘게임 체인저’로 평가되는 이유다.